Permanence & Definition: Safe High Yield Capital Creation in Your Portfolio

Traditional Fixed Income investors are faced with a true conundrum today. The investor that I am referring to is one who would ordinarily have their portfolio weighted more toward fixed income, i.e., bonds, CD's, preferred stock, dividend stocks, etc., than equities. Either due to age and a need to preserve capital or an aversion to the risk present in the equity markets, many seek the comfort of asset classes that are not as volatile and provide a known yield like the coupon payable on a treasury bond or bank issued certificate of deposit.

Here's the problem. Interest rates determine the yield payable on the above mentioned asset classes and as we all know, thanks to the credit crisis in 2008-2009, interest rates have been suppressed by the Federal Reserve and other central banks around the world to spur growth. That's great if you are a borrower but tragic if you are a saver.

Let's keep the focus on the 10 Year Treasury Bond. The 10 Year T-Bond is known as the risk-free-rate globally. Treasury Bonds are backed by the full faith and credit of the US Treasury (a subject of great conjecture and debate lately but a discussion for another day) and represent the most stable investment available. Currently, T-Bonds are offering a coupon (the interest payable on the Bond's face) of around 2.5% payable semi-annually.

So, if you purchase a T-Bond at a Par Value of $1,000, you will receive two interest checks per year of $125. Individual circumstances appertaining, after you apply your individual tax rate and the effect of increases in the cost of living, you are most likely barely treading water with your dollar's ability to hold its value at a zero real return.

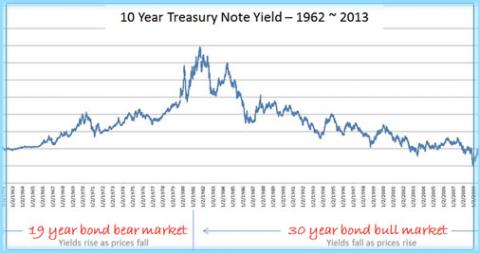

Furthermore, the movement of interest rates are the primary driver of the real value of a bond. In other words in the simplest terms, as rates rise, bonds trade at a discount to par and as rates fall, bonds trade at a premium to par. If you own a 2.50% coupon T-Bond and rates rise to 3.50%, one would expect to purchase your bond from you at a discount in order for there to be a compelling value against buying a new issue bond at 3.50%.

With interest rates at their historical low of basically zero, interest rates have nowhere to go but up as the global economy recovers. This will unfortunately cause pain to many bond holders if they have or want to liquidate their positions. It should be noted that if your intent is to harvest the yield until the bonds mature, none of this matters. But if your intent is not only to preserve but grow your capital base in a conservative, risk averse fashion, asset allocation has become very difficult.

Many who have grown tired of watching their money languish on the sidelines in money market accounts making nothing while the stock market has leapt out of its proverbial shoes have been forced to jump on the equity band wagon as it has by attrition become the only game in town.

So what do you do? The stock market seems to be setting new, all-time highs on a daily basis so that whole "Buy Low/Sell High" proposition is upside down and the fixed income market is facing perhaps a multi-decade bear market. To say the least, putting money to work in today's markets is fraught with peril and uncertainty.

Coming back to the title of this article, Permanence and Definition are but two attributes of an asset class that can help you circumvent some of the market risks you are facing. The asset class to which I am referring is Senior Life Settlements.

Senior Life Settlements are an attractive alternative fixed income asset class. A Senior Life Settlement is a life insurance contract on a senior citizen (age 75 or older) that is no longer wanted, needed or affordable. Senior Life Settlements are sold at an amount greater than the surrender value offered by the carrier but less than the face amount. The investor becomes the new owner and takes responsibility for the payment of the premiums until the contract matures (that is a nice way of saying until the insured person passes away). At maturity, the investor receives the death benefit from the insurance contract. The difference between the purchase price of the Senior Life Settlement contract plus the premiums paid is the investors Total Projected Yield. The Total Projected Yield to the investor at maturity will equal 65%.

Let's say that your total holding period for a portfolio of Senior Life Settlements is 6 years. To calculate your annual rate of return, divide 65% by 6 years which equals 10.83%. Be mindful that the annual yield can only be calculated after the maturity is known because human longevity is incalculable.

The important point to note in this limited forum is that Senior Life Settlements are non-correlated to the markets. Interest rates, geo-political and other volatility inducing events are unimportant to the outcome of a Senior Life Settlement investment. The only trigger affecting the investor's receipt of the yield is the life span of the settlor (the insured).

The investment/credit risk profile of a Senior Life Settlement falls between a Treasury Bond and a bank issued Certificate of Deposit. A Senior Life Settlement is not as safe as a Treasury Bond because it is not backed by the Full Faith and Credit of the US Treasury but the US Legal Reserve Life Insurance Carriers have higher credit ratings than banks. Given the equity market like yield of this asset class, Senior Life Settlements are an attractive alternative to other market based instruments.